Download PDF Excerpt

Rights Information

Making Sustainability Work 2nd Edition

Best Practices in Managing and Measuring Corporate Social, Environmental, and Economic Impacts

Marc Epstein (Author) | John Elkington (Foreword by) | Adriana Rejc Buhovac (Author) | Herman B. "Dutch" Leonard (Foreword by)

Publication date: 03/06/2014

Offers a complete guide to the details of implementing and measuring the impact of CSR initiatives

Most companies today have some commitment to corporate social responsibility, but implementing these initiatives can be particularly challenging. While a lot has been written on ethical and strategic factors, there is still a dearth of information on the practical nuts and bolts. And whereas with most other organizational initiatives the sole objective is improved financial performance, sustainability broadens the focus to include social and environmental performance, which is much more difficult to measure.Now updated throughout with new examples and new research, this is a complete guide to implementing and measuring the effectiveness of sustainability initiatives. It draws on Marc Epstein's and new coauthor Adriana Rejc Buhovac's solid academic foundation and extensive consulting work and includes best practices from dozens of companies in Europe, Asia, North America, South America, Australia, and Africa. This is the ultimate how-to guide for corporate leaders, strategists, academics, sustainability consultants, and anyone else with an interest in actually putting sustainability ideas into practice and making sure they accomplish their goals.

- A comprehensive guide to implementing and evaluating corporate sustainability initiatives

- Combines a thorough grounding in the latest research with the best practices of 100 organizations worldwide, including prominent companies such as Canon, Coca-Cola, Dell, FedEx, General Mills, Johnson & Johnson, Nestle, Starbucks, Warner Brothers

The best practices in corporate social responsibility (CSR) are no longer the exclusive domain of companies like Ben & Jerry's or the Body Shop; now even companies like GE and Wal-Mart are making significant financial and organizational commitments to social and environmental issues. But senior executives are realizing that implementing sustainability is particularly challenging. While a lot has been written on ethical and strategic factors, there is a dearth of information on the practical nuts and bolts of implementation and virtually nothing on how to measure the results.

In Making Sustainability Work, Marc Epstein builds on his influential and highly respected previous work to produce the ultimate how-to guide for corporate leaders, strategists, academics, sustainability consultants, and anyone else with an interest in actually putting sustainability ideas into practice.

Find out more about our Bulk Buyer Program

- 10-49: 20% discount

- 50-99: 35% discount

- 100-999: 38% discount

- 1000-1999: 40% discount

- 2000+ Contact ( bookorders@bkpub.com )

Offers a complete guide to the details of implementing and measuring the impact of CSR initiatives

Most companies today have some commitment to corporate social responsibility, but implementing these initiatives can be particularly challenging. While a lot has been written on ethical and strategic factors, there is still a dearth of information on the practical nuts and bolts. And whereas with most other organizational initiatives the sole objective is improved financial performance, sustainability broadens the focus to include social and environmental performance, which is much more difficult to measure.Now updated throughout with new examples and new research, this is a complete guide to implementing and measuring the effectiveness of sustainability initiatives. It draws on Marc Epstein's and new coauthor Adriana Rejc Buhovac's solid academic foundation and extensive consulting work and includes best practices from dozens of companies in Europe, Asia, North America, South America, Australia, and Africa. This is the ultimate how-to guide for corporate leaders, strategists, academics, sustainability consultants, and anyone else with an interest in actually putting sustainability ideas into practice and making sure they accomplish their goals.

- A comprehensive guide to implementing and evaluating corporate sustainability initiatives

- Combines a thorough grounding in the latest research with the best practices of 100 organizations worldwide, including prominent companies such as Canon, Coca-Cola, Dell, FedEx, General Mills, Johnson & Johnson, Nestle, Starbucks, Warner Brothers

The best practices in corporate social responsibility (CSR) are no longer the exclusive domain of companies like Ben & Jerry's or the Body Shop; now even companies like GE and Wal-Mart are making significant financial and organizational commitments to social and environmental issues. But senior executives are realizing that implementing sustainability is particularly challenging. While a lot has been written on ethical and strategic factors, there is a dearth of information on the practical nuts and bolts of implementation and virtually nothing on how to measure the results.

In Making Sustainability Work, Marc Epstein builds on his influential and highly respected previous work to produce the ultimate how-to guide for corporate leaders, strategists, academics, sustainability consultants, and anyone else with an interest in actually putting sustainability ideas into practice.

Foreword from the First Edition--John Elkington, SustainAbility Herman B Dutch Leonard, Harvard Business School

Preface

Introduction: Improving sustainability and financial performance in global corporations

Why it's important

Managing corporate sustainability

The Corporate Sustainability Model

Background to this book

Making sustainability work: an overview of the revised book

And finally

1--A new framework for implementing corporate sustainability

What is sustainability?

Identify your stakeholders

Be accountable

Corporate Sustainability Model Summary

2--Leadership, organizational culture, and strategy for corporate sustainability

Board commitment to sustainability

CEO commitment to sustainability

Leadership and global climate change

The role of the corporate mission and vision statements

The role of organizational culture

Developing a corporate sustainability strategy

Thinking globally

Voluntary standards and codes of conduct

Working with government regulations

Social investors and sustainability indices

Summary

3--Organizing for sustainability

The challenge for global corporations

Involve the whole organization

Information flow and a seat at the table

Outsourcing

Philanthropy and collaboration with NGOs

Summary

4--Costing, capital investments, and the integration of sustainability risks

The capital investment decision process

Capital budgeting in small and medium enterprises

Costs in the decision-making process

Costing systems

Risk assessment

Summary

5--Performance measurement, evaluation, and reward systems

Performance measurement and evaluation systems

Incentives and rewards

Strategic performance measurement systems

Shareholder value analysis

Summary

6--The foundations for measuring social, environmental, and economic impacts

The concept of value

Methodologies for measuring social, environmental, and economic impacts

Methodologies for measuring sustainability and political risks

Summary

7--Implementing a social, environmental, and economic impact measurement system

Mapping the actions that drive performance

Sustainability performance metrics

Engage with your stakeholders

Measuring reputation

Measuring risk

Measuring social, environmental, and economic impacts

Summary

8--Improving corporate processes, products, and projects for corporate sustainability

Organizational learning: the new battleground?

Improving sustainability performance

Reducing social, environmental, and economic impacts

Involve the supply chain

Internal reporting

Summary

9--External sustainability reporting and verification

Standards for sustainability reporting

Industry guidance on sustainability reporting

Let everyone know how you're doing

External disclosure of sustainability performance measures

Verifying sustainability performance and reporting Internal sustainability audits

External sustainability audits

Summary

10--The benefits of sustainability for corporations and society

Make sustainability work

Use the Corporate Sustainability Model to improve performance

Create opportunities for innovation

A last word

Endnotes

Bibliography

Index

CHAPTER 1

A new framework for implementing corporate sustainability

With growing sensitivity toward social, environmental, and economic issues and shareholder concerns, companies are increasingly striving to become better corporate citizens. Executives recognize that long-term economic growth is not possible unless that growth is socially and environmentally sustainable. A balance between economic progress, social responsibility, and environmental protection, sometimes referred to as the triple bottom line, can lead to competitive advantage.1 Through an examination of processes and products, companies can more broadly assess their impact on the environment, society, and economy, and find the intersection between improving sustainability impacts and increased long-term financial performance. To aid executives in achieving sustainability, this chapter will:

• Define the principles of sustainability

• Identify important stakeholder relationships

• Introduce a framework—the Corporate Sustainability Model—to guide managers in measuring and managing sustainability performance. This framework will be the basis for the remainder of the book and provides a tool for the implementation of corporate sustainability and the evaluation of corporate impacts

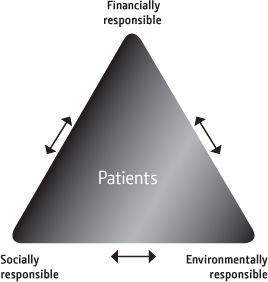

The evaluation of social, economic, and environmental impacts of organizational actions is necessary to make effective operational and capital investment decisions that positively impact organizational objectives and satisfy the objectives of multiple stakeholders. In many cases, reducing these impacts increases long-term corporate profitability through higher production yields and improved product quality. Novo Nordisk, the global Danish-based healthcare company specializing in diabetes care, strives to conduct its business in a financially responsible (profitable for the long-term), socially responsible (patients first), and environmentally responsible (doing more with less) way. The aim is to ensure long-term profitability by minimizing any negative impacts from business activities and maximizing the positive footprint from its global operations: improved health, employment, economic prosperity, and social equity (see Fig. 1.1).

FIGURE 1.1 Novo Nordisk’s triple bottom line business principle

Source: Novo Nordisk (2012) Annual Report

There is growing interest among the business community in the development and implementation of sound, proactive sustainability strategies, including significantly increased stakeholder engagement. The financial payoff of a proactive sustainability strategy can be substantial.2 By addressing the nonfinancial aspects of business, companies can improve the bottom line and earn superior returns. The Dow Chemical Company, a global diversified chemical company, focuses on manufacturing efficiency inside the company while maximizing the contributions of Dow products to improve efficiency and expand affordable alternatives. Dow’s manufacturing energy intensity has improved more than 40% since 1990, saving the company a cumulative US$24 billion. Dow is committed to bringing solutions to the challenge of climate change by producing products that help others reduce greenhouse gas emissions, such as lightweight plastics for automobiles and insulation for energy efficient homes and appliances.3

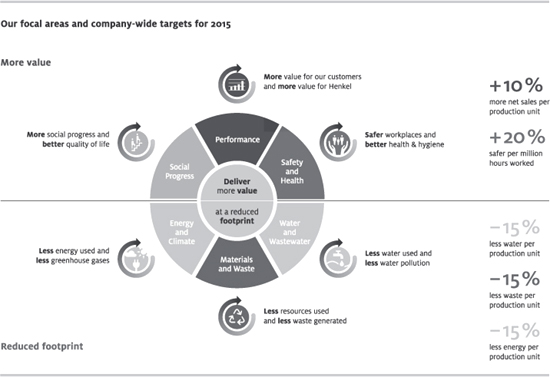

Henkel International, a German-based manufacturer of laundry and homecare products, beauty care, and adhesive technologies, has developed a sustainability strategy to create more value for its customers and consumers, for the communities it operates in, and for the company—at a reduced ecological footprint. Henkel concentrates its activities along the value chain on six focal areas that reflect the challenges of sustainable development as they relate to Henkel’s operations. Figure 1.2 presents Henkel’s six focal areas with five-year targets for 2015. Focal areas are subdivided into two dimensions—“more value” and “reduced footprint”. To accomplish these, the company uses innovations, products, and technologies, but recognizes that these dimensions must be ever-present in the minds and day-to-day actions of around 47,000 employees.

FIGURE 1.2 Henkel’s six focal areas in sustainability performance

Source: Henkel (2012) Sustainability Report

To become a leader in sustainability, it is important to articulate what sustainability is, develop processes to promote sustainability throughout the corporation, measure performance on sustainability, and ultimately link this to corporate financial performance. Corporate citizenship is an important driver for building trust, attracting and retaining employees, and obtaining a “license to operate” within communities. However, corporate citizenship is much more than charitable donations and public relations—it’s the way the company integrates sustainability principles with everyday business operations and policies, and then translates it all into bottom-line results.

For sustainability to be long-lasting and useful, it must be representative of and integrated into day-to-day corporate activities and corporate performance. If it is seen only as an attempt to provide effective public relations, it does not create long-term value and can even be a value destroyer. The key is integrating sustainability into business decisions, and identifying, measuring, and reporting (both internally and externally) the present and future impacts of products, services, processes, and activities. In fact, this book is all about the integration of sustainability into corporate operations to simultaneously achieve increases in social, environmental, economic, and financial performance.

What is sustainability?

To help understand what sustainability is in the context of corporate responsibility, we have broken it down into nine principles (see Table 1.1).4 These principles have three attributes:

1. They make the definition of sustainability more precise

2. They can be integrated into day-to-day management decision processes and into operational and capital investment decision-making

3. They can be quantified and monetized

These nine principles of sustainability will be used as a foundation throughout this book. They highlight what is important in managing stakeholder impacts (i.e. the impact of company products, services, processes, and other activities on corporate stakeholders).

Although we are presenting in Table 1.1 a broad definition of sustainability, this book focuses on the criteria that are usually included in sustainability discussions, analyses, measurements, and reports—social, environmental, and economic. So, though the principles of ethics and governance, for example, are important aspects of sustainability, they are not the focus of most corporate applications of corporate social responsibility or sustainability. But the discussion of systems, structures, performance measures, culture, and so forth necessary for implementation can be easily adapted to improve performance on all nine principles.5 Further, the formal and informal organizational processes described in this book should be applied to all of these principles.

1. Ethics |

The company establishes, promotes, monitors, and maintains ethical standards and practices in dealings with all of the company stakeholders |

2. Governance |

The company manages all of its resources conscientiously and effectively, recognizing the fiduciary duty of corporate boards and managers to focus on the interests of all company stakeholders |

3. Transparency |

The company provides timely disclosure of information about its products, services, and activities, thus permitting stakeholders to make informed decisions |

4. Business relationships |

The company engages in fair-trading practices with suppliers, distributors, and partners |

5. Financial return |

The company compensates providers of capital with a competitive return on investment and the protection of company assets |

6. Community involvement/economic development |

The company fosters a mutually beneficial relationship between the corporation and community in which it is sensitive to the culture, context, and needs of the community |

7. Value of products and services |

The company respects the needs, desires, and rights of its customers and strives to provide the highest levels of product and service values |

8. Employment practices |

The company engages in human-resource management practices that promote personal and professional employee development, diversity, and empowerment |

9. Protection of the environment |

The company strives to protect and restore the environment and promote sustainable development with products, processes, services, and other activities. |

TABLE 1.1 The broad definition of sustainability performance—nine principles

Source: Epstein and Roy (2003) “Improving Sustainability Performance”

1. Ethics

Ethical companies establish, promote, monitor, and maintain fair and honest standards and practices in dealings with all of the company stakeholders and encourage the same from all other stakeholders, including business partners, distributors, and suppliers. To follow this principle, a company needs to place particular emphasis on human rights and diversity to ensure that workers are treated fairly. This means that, although a company has to adhere to local laws, its ethical practices will often necessitate standards far in excess of industry, international, national, and local guidelines or regulations.

Ethical companies set high standards of behavior for all employees and agents, and have in place effective systems for monitoring, evaluating, and reporting on how the company does business. The reporting of ethical violations to appropriate authorities is also actively promoted.

Ethical companies create codes of conduct, develop ethics education programs, and honor internationally recognized human rights programs.

2. Governance

The governance principle is a commitment to manage all resources conscientiously and effectively, recognizing the fiduciary duty of corporate boards and managers to focus on the interests of all company stakeholders. This duty is of primary importance and is superior to the interests of management. The company follows practices of fair process and seeks to enhance both financial and human capital while balancing the interests of all of its stakeholders.

The company encourages the achievement of its mission while being sensitive to the needs of its various stakeholders. Its mission must be clearly stated and widely understood, and must recognize the interests of multiple stakeholders. The company must have a strategy and performance metrics that are consistent with its mission. The mission, strategy, policies, practices, and procedures are communicated openly and clearly to employees. Decision-making processes are engrained within this principle as performance is directly related to a particular course of action taken by the company.

Companies that value governance evaluate the CEO and senior management on financial and nonfinancial performance and have a board structure that represents a wide range of stakeholder views.

3. Transparency

While the governance principle relates to internal management issues, the transparency principle is about disclosure of information to company stakeholders. Transparent companies provide full disclosure to existing and potential investors and lenders of fair and open communication related to the past, present, and likely future financial performance of the company.

Transparent companies broadly identify their stakeholders. Indeed, companies embracing this principle recognize that they are accountable to internal and external stakeholders, understanding both their informational needs and their concerns about the company’s effects on their lives.

4. Business relationships

Companies must encourage reciprocity in their relationships with suppliers, by treating them as valued long-term partners in enterprise, enlisting their talents, loyalty, and ideas. Companies endorse long-term stable relationships with suppliers in return for quality, performance, and competitiveness. Companies select their suppliers, distributors, joint-venture partners, licensees, and other business partners not only on the basis of price and quality but also on social, ethical, and environmental performance.

Companies that embrace this principle set specific targets for utilizing indigenous, disadvantaged, or minority-owned businesses and use their purchasing power to encourage suppliers to improve their own social, environmental, and economic practices.

5. Financial returns to investors and lenders

The company compensates providers of capital with a competitive return on investment and the protection of company assets. Company strategies promote growth and enhance long-term shareholder value. The interests of investors and lenders must be explicitly recognized and companies must develop formal mechanisms to foster an ongoing dialogue with their investors. However, though improved financial results are a natural product of creating value for customers, employees, and other stakeholders, the company is committed to balancing the interests of all stakeholders.

6. Community involvement and economic development

Increasingly, companies recognize that it is in the best long-term interest of both the company and the community to improve the community, community resources, and the lives of its members. Thus, the company fosters a mutually beneficial relationship between the corporation and the community in which it is sensitive to the culture, context, and needs of the community. The company plays a proactive and cooperative role in making the community a better place to live and conduct business.

Companies that value community involvement and economic development collaborate with community members who promote rigorous standards of health, education, safety, and economic development.

7. Value of products and services

This principle requires companies to specify their relation and obligations to their customers. A proactive stance on this principle requires the company to respect the needs, desires, and rights of its customers and ultimate consumers, and to provide the highest levels of product and service values, including a strong commitment to integrity, customer satisfaction, and safety.

Companies create explicit programs to assess the impacts on their stakeholders of the products and services they provide.

8. Employment practices

Companies must decide on the type of management practices they want to engage in. Adopting this principle means that companies engage in management practices that promote personal and professional employee development, diversity, and empowerment. Companies regard employees as valued partners in the business, respecting their right to fair labor practices, competitive wages and benefits, and a safe, family-friendly work environment.

Indeed, companies adopting this principle recognize that concern for and investing in employees is in the best long-term interests of the employees, the community, and the company. Thus, companies strive to increase and maintain high levels of employee satisfaction and respect international and industry standards for human rights. To do this they offer programs such as tuition reimbursement, family leave time, day care, and career development opportunities.

9. Protection of the environment

To follow this principle, companies must define their commitment to the natural environment. For proactive companies, it means striving to protect and restore the environment and promoting sustainable development with products, processes, services, and other activities. Companies must be committed to minimizing the use of energy and natural resources, and decreasing waste and emissions. At a minimum, the company fully complies with all existing international, national, and local regulations and industry standards regarding emissions and waste. It strives for continuous improvement in the efficiency with which it uses all forms of energy, in reducing its consumption of water and other natural resources, and its emissions into air, water, and land of hazardous substances. It also entails a commitment to maximize the use and production of recycled and recyclable materials, the durability of products, and to minimize packaging.

Increasingly, companies have recognized that sustainability values and principles are important for long-term corporate profitability and are using them to define their sustainability strategies. Alcatel-Lucent, a French-based global communications industry leader, focuses on three core sustainability priorities: extreme green innovation; employees; and digital inclusion. A core element of Alcatel-Lucent sustainability strategy and day-to-day businesses are the following three values:

• “We take a zero tolerance stance on compliance violations and reinforce full integrity in every business action from every employee, treating each other with respect and empathy

• We collaborate and do business only with partners, suppliers, contractors and subcontractors who share and support our values. We commit to regularly and thoroughly assessing their performance and partnering to ensure improvement

• “We commit to engaging with pride and passion as citizens of the communities where we do business around the globe”6

However, identifying the values or dimensions of sustainability in a theoretical way is only the first step in improving corporate accountability and long-term profitability. The values of the company need to align with the values of its important stakeholders; so stakeholder identification is the next step.

Identify your stakeholders

In managing sustainability, stakeholder value (a significantly broader concept than shareholder value) is critical. How an organization chooses to define its stakeholders is an important determinant of how stakeholder relations are considered in sustainability decision-making and how stakeholder reactions are managed. Some definitions cover those individuals who can either be affected by or affect the organization, while others require that a stakeholder be in a position to both influence and be influenced by organizational activities.7 Additionally, there are core stakeholders and fringe stakeholders. Core stakeholders are those that are visible and are able to impact corporate decisions due to their power or legitimacy. Fringe stakeholders, on the other hand, are disconnected from the company because they are remote, weak, or currently disinterested.8 Typical stakeholders include shareholders, customers, suppliers, employees, regulators, and communities.

Few companies have advanced their stakeholder engagement on sustainability as quickly and effectively as Dell, an American multinational computer technology corporation. The company realized long ago that engaging with stakeholders adds enormous value to their sustainability efforts. In addition to the usual groups such as suppliers, NGOs (nongovernmental organizations) and industry consortiums, Dell has benefited enormously from the perspectives of peers and competitors, government agencies, investment groups, academics, faith-based groups, and customers. However, the company has found that about 10–12 different organizations is the optimum number of participating stakeholders on any particular issue. Beyond that, some stakeholders feel their opinions are not being heard or considered.9

Relationships with stakeholders should evolve over time. These relationships often go through the following four stages:

1. Awareness. At this stage stakeholders know that the company exists. Companies will want to communicate with these stakeholders by providing them with more information about the company so that they can begin to appreciate the company’s mission and values

2. Knowledge. Stakeholders have begun to understand what the company does, its values, strategy, and mission. During this stage, companies want to provide stakeholders with information to make decisions. Customers want to know how the organization’s products meet their needs, employees need to understand organization structure and systems, and suppliers want to understand what the company needs from them

3. Admiration. Once stakeholders have gained knowledge about the company, trust needs to be developed. This is the stage where stakeholders will develop commitment toward the company

4. Action. Companies are now taking action to collaborate further with stakeholders. Customers refer business, investors recommend the stock, and employees are willing to take on greater responsibility10

To move toward a more complete understanding of sustainability and a further integration of social, environmental, and economic issues into core business strategy and operational decisions, sustainability values and organizational stakeholders must be identified and specified. (Stakeholder engagement and the measurement of stakeholder reactions are discussed in more depth in Chapter 7.) Many constituents have a legitimate stake in company activities and, therefore, a variety of interests and opinions are important in developing sustainability strategies. The long-term value of a company is influenced by the knowledge and commitment of its employees and its relationships with investors, customers, and other stakeholders.11 Additionally, corporate stakeholders are demanding increased information about corporate governance and the impact of corporate activities on society. This call for corporate transparency requires companies to account for their social, environmental, and economic impacts.

This is particularly critical since the aftermath of Enron, when ethical obligations and accountability, including social, environmental, and economic responsibility, transparency, and proactive engagement with stakeholders became a higher priority for top executives. In many corporations, the operational and reputational effects of negative social, environmental, and economic impacts, along with financial analysts’ concerns of increased risk leading to future liabilities, have caused stock prices to be lower and costs of capital to be higher than in comparable more socially, environmentally, and economically responsible companies. Because of the increased scrutiny and effects that it can have on the bottom line, many corporations are focusing more on improving their reputation for effective management of social, environmental, and economic impacts.

Be accountable

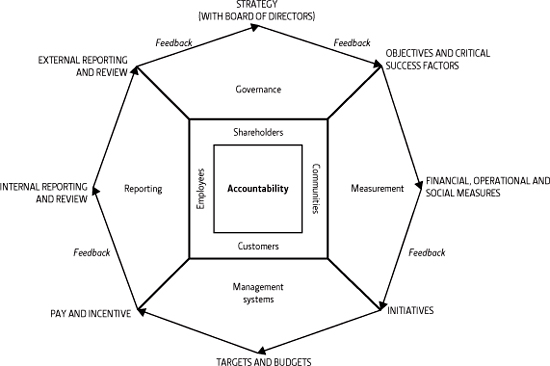

To better integrate a broader set of stakeholder concerns into management decisions, consideration of impacts and recognition of the importance of accountability is necessary. In Counting What Counts: Turning Corporate Accountability to Competitive Advantage, along with Bill Birchard, Marc Epstein developed an accountability cycle (Fig. 1.3) which defines four approaches to becoming an accountable organization.12 The four primary elements are:

1. Improved corporate governance centered around two essential conditions: director independence and enhanced board performance. Both are necessary to enable the board to make better decisions and to stimulate continuous improvement in company performance

2. Improved measurements that include operational and social measures of performance along with a broadened set of financial metrics that include both leading and lagging indicators

3. Improved reporting to a broad set of internal and external stakeholders of information relevant to decisions. This begins with internal reporting to managers and the selection of various voluntary disclosures to supplement the mandatory external disclosures that are currently the primary content of corporate reports

4. Improved management systems to drive these improvements through corporate culture and change the way managers make decisions to improve both corporate accountability and corporate performance

The model integrates both internal and external reporting, along with a broader set of measures, and provides a mechanism to link social, environmental, and ethical concerns to financial performance. It provides broad guidance for the integration of social concerns into day-to-day management decisions and does so in a format that examines the relevance of social and other leadership issues to overall corporate performance. It also provides a framework of corporate accountability that can be used as a foundation for the implementation of a sustainability strategy.

FIGURE 1.3 The accountability cycle

Source: Epstein and Birchard (1999) Counting What Counts

Corporate Sustainability Model

So, to have an effective sustainability strategy, it is critical that managers understand:

• The causal relationships between the various alternative actions that can be taken

• The impact of these actions on sustainability performance

• The likely reactions of the corporation’s various stakeholders to sustainability performance

• The potential and actual impacts on financial performance

By carefully identifying these interrelationships and by establishing relevant performance metrics to measure success, a company can improve operational decision-making and make the “business case” for a sustainability strategy by better linking it with the impacts of the strategy on both the company, society, and the environment.

However, effective implementation and measurement of success are significant challenges. Companies must find ways to motivate employees to focus on sustainability issues while managing sustainability and financial outcomes simultaneously. Additionally, to get adequate resources for the strategy, senior sustainability managers need better ways to measure the payoffs of these actions and programs. General corporate and business unit managers often request an analysis of the payoffs of proposed expenditures so that the resource allocation decisions can be made using the same ROI (return on investment) model that is used throughout the organization. Therefore, we need more guidance in understanding the drivers and measures of success.

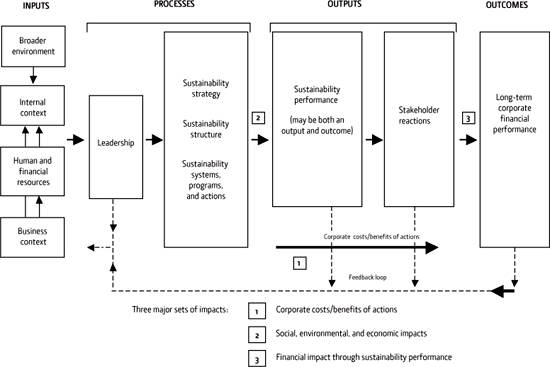

The Corporate Sustainability Model (see Fig. 1.4) uses the social, environmental, and economic dimensions of sustainability as its foundation.13 The model describes the drivers of corporate sustainability performance, the actions that managers can take to affect that performance, and the consequences of those actions on corporate environmental, social, economic, and financial performance. By more carefully understanding both the drivers of sustainability performance and the impacts of that performance on the various corporate stakeholders it is easier to integrate the information into day-today operational decisions.

The inputs of the model include the broader external context (regulatory, geographical), internal context (mission, vision, strategy, structure, systems), the business context (industry sector, customers, products), and the human and financial resources. These guide the decisions of leaders and the processes that the organization undertakes to improve its sustainability. They provide a foundation for understanding the complex factors leaders should consider and often take the form of constraints that must be addressed.

After evaluating the inputs and their likely effects on sustainability and financial performance, leaders can develop the appropriate processes to improve sustainability. The sustainability strategy, structure, systems, programs, and actions have three major ultimate sets of impacts: corporate financial costs and benefits of actions; social, environmental, and economic impacts (sustainability performance); and long-term financial impacts through sustainability performance.

The managerial actions taken lead to sustainability performance (positive or negative) and stakeholder reactions, ultimately affecting long-term corporate financial performance. Also included in the model are continual feedback loops that leaders can use to evaluate and improve corporate strategies. Managers should customize this general framework to reflect their particular industry, geographical, internal, or external business context. They must map a corporate performance framework that reflects their specific concerns and interests in sustainability performance and provides rewards for supportive managerial actions.

FIGURE 1.4 Corporate Sustainability Model

A fundamental aspect of this framework is the distinction between intermediate results (outputs) and financial outcomes. In Figure 1.4:

• Arrow 1 portrays processes that have immediate and identifiable costs and benefits that affect long-term corporate financial performance

• Arrow 2 shows the impact of the various inputs and processes on sustainability performance

• Arrow 3 shows how corporate financial performance is impacted by stakeholder reactions to corporate sustainability performance

Therefore, intermediate outputs, such as environmental, social, and economic performance (but also public image, employee hiring, customer reactions, and market share) must be monitored to determine the effectiveness of sustainability management practices.

Arrow 3 depicts what is often termed the “business case” for sustainability or corporate social responsibility. Whereas arrow 2 portrays the effect of sustainability actions on social, environmental, and economic performance, arrow 3 reflects how, through stakeholder reactions, social, environmental, and economic performance affects financial performance. Thus, sustainability performance should be seen as both an intermediate output and as an outcome. That is, it is important to understand, measure, monitor, and manage sustainability performance because of concern for societal, environmental, and economic impacts and for long-term corporate financial performance.

So, the inputs, processes, and outputs are all critical elements of the process to drive the outcome of corporate profitability. In the discussion below, the details of these inputs, processes, outputs, and outcomes are further explored. They are then discussed in greater detail in the chapters that follow.

Inputs

Broader external context

The local and global broader external context significantly affects the choices a corporation makes regarding the formulation and implementation of sustainability actions. Pressure is exerted by government regulations for corporations to follow minimum standards of sustainability performance: for example, hazardous and other waste disposal regulations, pollution standards, nondiscrimination laws, and regulations governing working conditions. Regulatory pressure may vary by geographic region, with regulatory pressures typically stronger in some European and Asian countries. If these types of regulation are required by government, a corporation must respond effectively by developing a thorough sustainability plan. Additionally, the appropriate level of wages (living, minimum, or prevailing) and the desirability of the employment of children are issues that have caused significant dismay to many widely recognized companies.

Another external influence on a corporation’s choice of sustainability strategy is the marketplace for the corporation’s products and services. In studies of corporations operating in China and in Mexico, it was shown that corporations selling to customers in economies with a relatively stronger culture of sustainability performance outperformed their peer companies in terms of environmental performance.14 Additionally, some locations are more tolerant of pollution due to their topography and weather patterns, in addition to public reactions and the regulatory environment; and so a corporation must consider whether it wants to adapt sustainability strategies to locational differences.

In 2012, the US Securities and Exchange Commission (SEC) enacted a rule that represents an attempt to curtail human rights abuses in Africa through regulation of US public companies. The Conflict Minerals Rule requires companies to trace the conflict minerals (gold, tantalum, tin, and tungsten) in their supply chains. The SEC estimated that 6,000 US issuers will be directly affected by the rule. It also estimated the initial compliance costs of US$3 billion to US$4 billion as end users of the four conflict minerals attempt to find out whether their raw materials originated at mines run by warlords in the Democratic Republic of the Congo or its nine adjoining neighbors (Angola, Burundi, Central African Republic, the Republic of Congo, Rwanda, South Sudan, Tanzania, Uganda, and Zambia). The complexity and far-reaching effect of the new rule can be demonstrated by an estimate made by Hewlett-Packard (HP), an American multinational information technology corporation, that about 1,000 suppliers in its chain ultimately provide a product to HP that may contain one of the conflict minerals. Each supplier will be asked to do its part in the due diligence process required by the new rule.

Companies making public anti-conflict minerals statements include Intel, Philips, and Samsung. Intel, a multinational semiconductor chip maker corporation, set a goal for 2013 to manufacture the world’s first verified, conflict-free microprocessor. Philips, a Dutch multinational engineering and electronics conglomerate, has committed not to purchase materials it knows finance armed groups in the affected countries. Samsung, a multi-faceted family of businesses, including high-tech electronics manufacturing and digital media, prohibits the use in its business units of conflict minerals identified as sourced from conflict mines in the affected countries. Some companies want to go beyond the minimum of complying and reporting and make a perhaps costly effort to make sure none of their materials come from mines run by warlords in the affected countries.15

Internal context

This comprises corporate and business unit missions, visions, strategies, structures, and systems; it is through the development and implementation of these that sustainability performance occurs. Thus, companies that are striving toward improved sustainability performance must examine the various sustainability elements that relate to their current strategies, and assess whether and how their corporate and business unit strategies will probably impact issues such as human rights, employee rights, and environmental protection.

Business context

Additional important considerations are the industry sector of the business, and the characteristics of customers and products. Companies that operate in high social and environmental impact industries, such as chemicals, oil, paper, and mining, may exhibit relatively poor performance in terms of sustainability elements such as consumption of natural resources, emissions, and health risk of their products or services compared to companies operating in other industries. The industry also impacts where companies focus their sustainability efforts. For example, oil and mining companies may focus more on environmental and health issues, while service-oriented companies may emphasize the social aspects of sustainability. Although all companies can improve their social, environmental, and economic impacts, some industries have greater opportunities and risks. These include companies with:

• High brand exposure (consumer products companies)

• Big environmental impact (oil companies, manufacturing)

• Natural-resource dependence (fish, food, forest products)

• Current exposure to regulations (hazardous materials, utilities)

• Increasing potential for regulation (automobiles, electronics)

• Competitive markets for talent (service sectors)

• Low market value (small-to-medium B2B [business to business] companies)16

Further, companies in different industries are exposed to widely different pressures from political institutions, customers, and community activists. These various pressures become important external drivers of corporate sustainability. Issues such as labor practices and environmental management exist in many industries and have been of increasing community concern. Company and industry codes of conduct are widely and rapidly being established in many industries, including those in the apparel, toy, and footwear industries. Many companies are now working together to establish global labor standards and common factory inspection systems.

Human and financial resources

Another important input is the resources constraint of the corporation. The corporation needs financial resources to implement the various sustainability programs and to pay and train sustainability staff. In addition, organizations need educated and trained individuals throughout the organization who can be sensitized to sustainability issues, along with staff who can be specifically dedicated to sustainability programs. The amount of financial and human resources allocated to sustainability will significantly impact the ability to implement sustainability programs.

Processes

Leadership

It is important for corporate leaders to consider all of these inputs if they want to formulate effective sustainability strategies. Research has shown that sustainability strategies are typically top-down and that the most effective ones are when top management is clearly committed to the strategy.17 Signals of this commitment are given through the way the strategy is communicated throughout the organization. Senior executives must be knowledgeable, support the organization, and effectively communicate the mission, vision, and strategy to the other members of the organization. The commitment of the board of directors and management encourages employees to act in ways that are compliant and consistent with company strategy. If leaders are not knowledgeable enough about sustainability to motivate their subordinates or institute the proper strategy, structure, or systems, then sustainability actions are unlikely to be successful. It is the responsibility of top leaders to create an environment that encourages sustainability. Verizon Communications, the large telecommunications company, has created a Corporate Responsibility and Workplace Culture Council to foster a culture that encourages sustainability. The council is chaired by the senior vice president for public policy development and corporate responsibility and by the vice president for workplace culture, diversity, and compliance, and consists of managers from each major business unit. It is responsible for identifying and addressing challenges associated with corporate citizenship in key areas, including accessible product design, broadband deployment, and supply chain and environmental management. Increasingly, companies also have committees of the board and other senior management committees devoted to issues of sustainability, and chief sustainability officers as members of the top management team. The importance of board and CEO leadership on sustainability is discussed in Chapter 2.

Sustainability strategy

Top management of some companies have neither developed a strategy for addressing environmental, social, and economic concerns nor developed any systematic way of evaluating or managing their sustainability impacts. In many cases, this lack of corporate responsiveness is evidence of companies that:

• Are crisis-prone rather than crisis-prepared

• May produce social, environmental, and economic impacts that have substantial future consequences involving increased costs, increased community concerns, increased legal claims, and damaged corporate reputation

• May decrease current and future corporate profitability through decreased potential revenues related to sustainability issues

Best practice companies pursue coherent sustainability strategies.

Guidance in the development of a sustainability strategy sometimes comes from governments and industries that have established minimum compliance standards or best practices for corporations. However, many companies go beyond a minimum compliance strategy. For example, prior to any industry standards, toy manufacturer Mattel established its own Global Manufacturing Principles for company-owned, -contracted, and -licensed facilities. These Global Manufacturing Principles provide a framework for its worldwide manufacturing practices requiring fair treatment of employees and protection of the environment.

Companies operating globally also have to choose whether to implement a global sustainability strategy or adapt it locally. As well as regulatory issues, cultural and environmental issues can complicate this decision. There are also significant implications here for corporate and sustainability structures and systems. The process of formulating a sustainability strategy is discussed more fully in Chapter 2.

Sustainability structure

Some companies narrowly view sustainability as an operations function responsibility for environmental performance, as a human resource function responsibility for labor performance, as a community affairs function for community interaction, and perhaps place responsibility in the legal department to ensure that the company is doing things “right,” which through a legalistic lens means according to the law or extant regulation. Companies that define sustainability as a legal issue, or as solely an operations, community affairs, or human resources issue, often find themselves in a reactive position regarding sustainability issues and are missing significant opportunities to more fully integrate sustainability into their business practices.

Companies need to leverage sustainability concerns throughout the organization. A study of Mexican firms found that sustainability outcomes were significantly improved when more than two departments had functional responsibility for sustainability performance.18 For example, at UPS, a global shipping company, health and safety managers are placed in each business unit to implement strategic safety initiatives. How to improve sustainability through organizational design is covered in Chapter 3.

Sustainability systems, programs, and actions

To drive a sustainability strategy through an organization, various management systems, such as product costing, capital budgeting, information, and performance evaluation, must be designed and aligned. Many companies have revised their performance measurement and evaluation systems to help gauge the sustainability performance of business units and company facilities. For example, Sony uses an intranet-based data system to collect sustainability information from its sites worldwide. Managers at each site input data on energy, water, waste, and other environmental costs, which allows Sony to track its impact on the environment. An effective performance evaluation system should integrate economic, environmental, and social objectives and reward the contributions of individuals, facilities, and business units toward meeting those corporate goals.

Many companies have been using the ISO 14001 environmental management system (EMS) for guidance on their environmental strategy. Indeed, a strong EMS is essential in helping companies systematically identify, measure, and appropriately manage their environmental obligations and risk. Without appropriate management systems, corporations may not reap all the benefits associated with sustainability performance. The alignment of strategy, structure, and management systems is essential in both coordinating activities and motivating employees.

The actions taken by the organization toward sustainability should be both internally and externally focused. Internally focused actions include:

• Labor practices and benefits programs

• Life-cycle analysis and design for environment

• Plant certifications

• Audits for social and environmental standards and practices

• Employee volunteer programs

• Training of employees—both sustainability training and also training to improve employee capabilities, integration of sustainability throughout the organization, and effective monitoring and reporting of results

Externally focused actions include:

• Philanthropy

• Community outreach programs

• Supplier certification requirements

• Supplier audits for workplace practices

• Public reporting of sustainability performance

Some actions are proactive, designed to impact sustainability performance (for example, life-cycle analysis), while others are implemented reactively to respond to the performance indicators and to stakeholder concerns. There is a growing body of research that reports that the most effective sustainability initiatives, in terms of impacting organizational performance, are those that are proactive rather than reactive.19 Many different plans and programs can be devised to improve sustainability performance. These can be minor changes of existing routines or radical new ways of doing business. They may include capital investments in new technologies, product or process redesign, or R&D spending. They may also include programs to promote ethical sourcing, workforce diversity, or more stringent codes of conduct in terms of labor practices.

Other plans and programs are directed at promoting a company’s sustainability performance to stakeholders. This requires both responsible actions and communication with the stakeholders. These stakeholder initiatives may include marketing efforts to promote social, environmental, and economic product features and lobbying efforts to governmental agencies related to social, environmental, and economic issues. The various systems, programs, and actions that can be used to promote sustainability are discussed thoroughly in Chapters 4 and 5.

Figure 1.5 lists some of the various organization processes that lead to success—including leadership, strategy, structure, and systems.

Leadership |

Strategy |

1. Show commitment from the top |

1. Develop a mission statement |

2. Scan business environment for potential risks and opportunities |

2. Consider global and local regulations, as well as voluntary standards |

3. Lead a cultural transformation |

3. Consider the impact of social investors |

Structure |

Systems |

1. Integrated throughout organization |

1. Costing and capital investment systems |

2. Effective use of human resources |

2. Risk management systems |

3. Manager access to top leadership |

3. Performance evaluation and reward systems |

4. Aligned with strategy |

4. Measurement systems |

|

5. Feedback systems |

|

6. Reporting and verification systems |

FIGURE 1.5 Sustainability actions leading to financial and sustainability success

Outputs

Sustainability performance

Companies, through their actions, can either improve or impair their sustainability performance. Sustainability performance is the social, environmental, and economic performance of a company and relates to the objectives that are important to the internal and external stakeholders of the organization. Performance goals and objectives are typically determined only after the organization has a clear understanding of its strategy, who its stakeholders are, and its relevant objectives. Social, environmental, and economic performance objectives typically relate to a broad set of company stakeholders and often address impacts that are at times broader and less tangible than financial performance objectives. This performance includes impacts as diverse as child labor, environmental emissions, product packaging, workplace practices, product quality, and so forth. It includes all of those impacts, both positive and negative, on the company’s various stakeholders. Because sustainability goals are often broad, organizations must focus on specific issues or areas of priority when assessing performance.

As mentioned earlier, sustainability performance can be both an intermediate output and a final outcome. In the development and evaluation of corporate sustainability strategies, companies typically attempt to improve their contributions by reducing negative corporate social, environmental, and economic impacts, increasing positive impacts, or both. Companies can view the social, environmental, and economic impacts as ultimate outcomes developed expressly for improving society with no explicit goal of improving profitability, or companies can attempt to improve their social, environmental, and economic impacts as an intermediate output to improving corporate profitability (often called the “business case”). In both considerations, it is important to:

• Measure sustainability performance and evaluate the effectiveness of programs

• Recognize the corporate impacts on society, the environment, and the economy

• Determine how the company can improve its contribution to society, the environment, the economy, and the corporation

The scope must be wide, with an extensive analysis of a broad set of stakeholders and impacts. Where current impacts or stakeholder reactions are low, companies must consider potential changes in impacts or likely future stakeholder reactions to current and future impacts. Chapters 6 and 7 deal with measurement of sustainability impacts.

Stakeholders’ reactions

Sustainability performance is converted to having an effect on corporate financial performance, through stakeholder reactions (again, see Fig. 1.4). Though critical, integrating consideration of all major stakeholder interests into day-to-day management decisions is a complex undertaking. Companies wishing to do so must broadly identify their stakeholders and the impacts of their products, services, and activities on those stakeholders. They must communicate openly to both internal and external stakeholders and implement the proper mechanisms to listen to their specific concerns through broad stakeholder identification and engagement.

Stakeholder reactions are an important component of the framework as they may significantly affect short-term revenues and costs and long-term corporate performance on many levels. Because gaining advantage through stakeholders has been recognized as a driver of strategic success, companies must identify the key stakeholder groups that are the primary drivers of their strategy, including shareholders, customers, suppliers, employees, and communities. Companies are now gaining lasting advantage through stakeholder relationships uniquely structured to provide strategic competitive advantage.

• Customers provide this advantage through loyalty and long-term purchasing. They can choose to buy more sustainability-positioned products or they can boycott products that are deemed to have negative social, environmental, or economic impacts

• Employees do the same when they commit to great service, innovation, and reliability. Potential employees can choose to work (or not work) for the company based on sustainability performance

• Regulators and communities can increase or decrease regulation, monitoring, and enforcement based on company performance

• Shareholders provide a lasting advantage when they provide long-term capital, and potential investors use sustainability performance as an important component in their investment decisions

Thus, companies must carefully consider likely stakeholder reactions in developing and implementing their sustainability strategy. The framework acknowledges that a company’s stakeholders can react to both sustainability performance and the actions taken to promote that performance. Methods of engaging stakeholders will be discussed in Chapter 7, while reporting sustainability performance to internal and external stakeholders is examined in Chapters 8 and 9.

Outcomes

Corporate financial performance

For most companies, the ultimate focus of sustainability strategies and programs must be short-term or long-term corporate financial performance. To effectively capture the impact on organizational performance, the outputs of the sustainability processes must be ultimately converted to monetary measures. The impacts of sustainability actions should include present and future benefits and costs, represented through additional revenues to the organization or a reduction in costs.

Extensive research has shown that improved corporate sustainability performance impacts financial results through both enhanced revenues and lower costs.20 Numerous studies have shown that consumers have a more favorable image of corporations that support causes that the consumers care about, and that many consumers report that they would switch brands based on social reputation.21 Revenues related to sustainability management initiatives can be positively impacted through reputational effects as well as through “green” marketing initiatives. Social initiatives undertaken by corporations also impact revenue streams and the level of annual expenditures for cause-related marketing is steadily increasing.

Costs are also positively influenced by sustainable management initiatives. Process improvements may lower costs of energy and water usage and decrease costs of waste handling and recycling. In an effort to reduce its environmental footprint while simultaneously boosting its bottom line, Alcoa’s Poços de Caldas refinery and smelter complex in Brazil reused or sold more than 30,000 metric tons of industrial byproducts for a com